Energy Shock To Clinical Cost: Mapping The Pharma Input Price Cascade

By Mathini Ilancheran, senior delivery lead - research, R&D, Beroe Inc.

The global pharmaceutical industry is experiencing a multi-layered cost escalation across APIs, excipients, polymers, clinical logistics, and laboratory consumables in Q1 2026. This escalation follows a defined geopolitical sequence: U.S. and Israel military engagement with Iran began on February 28, 2026, followed by disruption of the Strait of Hormuz on March 4, 2026, a critical chokepoint through which approximately 20% of global petroleum and significant LNG volumes transit.1,2

The disruption resulted in Brent crude rising above USD 120 per barrel within weeks, triggering upstream cost inflation across energy and petrochemical markets.2,3 In response, BASF Pharma Solutions announced a global price increase of up to 20% across excipients and selected APIs effective March 30, 2026.4,5 BASF also issued a USD 0.20/lb increase for caprolactam and polyamide polymers in North America effective April 1, 2026.6 Polyplastics -Evonik confirmed price revisions for polyamide and PEEK resins used in pharmaceutical packaging and device components.7

These developments collectively indicate the onset of a multi-layer price cascade, directly impacting clinical development cost structures.

Supplier Price Environment

The supplier landscape shows early-stage inflation concentrated in APIs, excipients, and engineering polymers, with additional categories entering the cycle. Confirmed supplier actions indicate that cost escalation has already begun, while watch-list suppliers suggest further increases in Q2 2026.

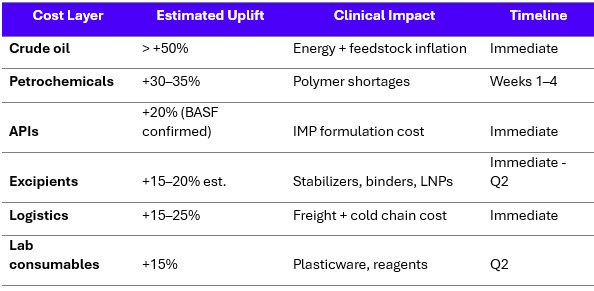

Table 1: Supplier Price Cascade Tracker (March - April 2026)

![]()

Sources: BASF, Fierce Pharma, SpecialChem

The initial pricing actions confirm that inflation is concentrated in upstream pharmaceutical inputs. APIs, excipients, and polymer-based materials are already seeing measurable increases, while lipid excipients, specialty chemicals, and lab consumables are expected to follow. This pattern is consistent with previous energy-driven cycles, where pricing spreads sequentially across the value chain.

Root Cause: Hormuz Disruption And Petrochemical Cascade

The cost escalation originates from disruption in the Strait of Hormuz, a key global energy and petrochemical transit route. The Middle East accounts for approximately 22% of global petrochemical supply, and around 84% of polyethylene capacity depends on the Strait for export.3,8

QatarEnergy declared force majeure and halted downstream production of polyethylene (PE), polypropylene (PP), and PVC following infrastructure disruptions.3,9 These materials are foundational to pharmaceutical packaging, delivery systems, and laboratory consumables.

A second transmission channel operates through India, which supplies approximately 47% of U.S. generic prescriptions and depends on the Strait for roughly 40% of its crude oil imports.5 This creates a direct link between energy cost inflation and API manufacturing costs. Similar exposure exists across other manufacturing hubs, including China, Japan, and South Korea, which are highly dependent on Gulf crude, LNG, and industrial feedstocks, extending cost pressures into petrochemical intermediates, packaging materials, and pharmaceutical inputs.10

Upstream Cost Cascade Into Clinical Development

The disruption propagates through a structured cost cascade, beginning with energy markets and extending into clinical development (Table 2). The data indicates a layered cost transmission mechanism. Energy price increases feed into petrochemical shortages, which then impact APIs, excipients, and logistics. The earliest effects are observed in APIs and freight, while lab consumables and secondary materials are expected to show stronger impact in Q2 2026.

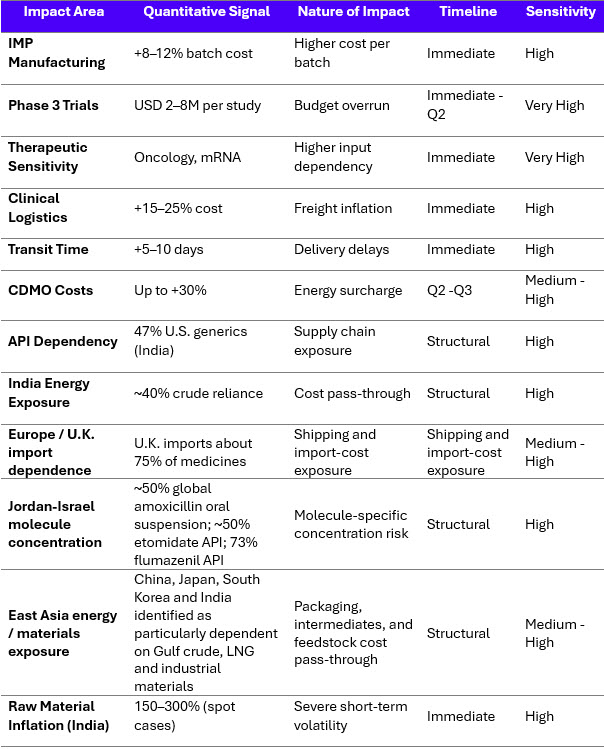

Table 2: Upstream Cost Cascade into Clinical Development

Sources: Beroe Analysis, BASF, CNBC, Fierce Pharma, IOM3/ICIS, ChemAnalyst

Clinical Development Impact Analysis

Clinical development is disproportionately affected due to reliance on global supply chains, high-value materials, and time-sensitive logistics. The below table 3 shows the Clinical Development Cost and Supply Impact Summary.

Table 3. Clinical Development Cost and Supply Impact Summary

Sources: Beroe Analysis, BASF, Fierce Pharma; India pharma reports (2026), CNBC

Clinical development costs are rising through three primary mechanisms: input cost inflation, logistics disruption, and geographic supply dependency. API and excipient price increases directly affect IMP manufacturing costs, while freight disruption introduces both cost escalation and delivery-delay risk.

India remains a major exposure point because Indian companies supplied 47% of U.S. generic prescriptions and API manufacturers there are facing solvent and key-starting-material pressure as inventories tighten. The U.K. and wider Europe are vulnerable through import dependence and shipping-route disruption, while the Jordan-Israel corridor represents a specific concentration risk for products such as amoxicillin oral suspension, etomidate, and flumazenil API.10,11

In addition, East Asian manufacturing hubs including China, Japan, and South Korea are highly exposed to Gulf energy and industrial-material flows, which can raise costs for petrochemical-derived intermediates, packaging, and clinical research consumables.12

Impact On Clinical Research & Lab Categories

The impact across clinical research categories varies based on dependency on logistics and petrochemical inputs. The below table 4 shows the dependency driver by category along with driver and impact.

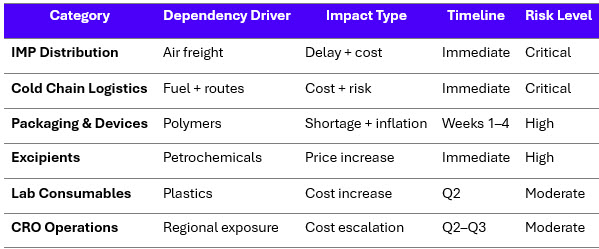

Table 4: Clinical Research and Lab Category Impact

Sources: Beroe Analysis, BASF, Fierce Pharma, IOM3

The highest exposure is concentrated in logistics-dependent and polymer-dependent categories. Clinical trial supply and cold chain logistics are affected immediately, while packaging materials and excipients show direct cost escalation. Laboratory consumables and CRO operations are expected to reflect cost pressure with a delay as contracts adjust.

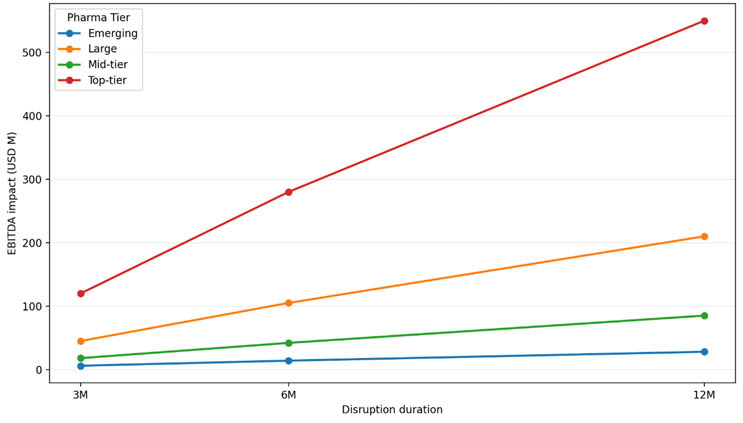

Estimated EBITDA Impact on Pharma – 2026

The cumulative effect of API, excipient, polymer, and logistics inflation is reflected in projected R&D cost escalation across pharma companies. The below model uses three main assumptions: a confirmed up to 20% increase in selected excipients and APIs from BASF, disruption-related logistics inflation and rerouting pressure affecting clinical supply chains, and reported 2025 R&D spend by pharma tier as the cost base.4,5,13

Under the base-case six-month disruption scenario, the model indicates approximately USD 280 million of incremental cost exposure for top-tier pharma, with proportionally lower but still material exposure for large, mid-tier, and emerging biopharma companies.

Estimated Incremental R&D Cost Exposure vs. Disruption Duration (2026)

Sources: Beroe Analysis

Plan For Cost Escalation

The March 2026 disruption has resulted in confirmed price increases across APIs, excipients, and polymers, alongside measurable increases in logistics and energy costs. BASF’s pricing actions and polymer supplier responses indicate that cost escalation is already underway and expanding across the pharmaceutical value chain.

The impact is most pronounced in clinical development due to reliance on global supply chains, specialized inputs, and time-sensitive logistics. Manufacturing costs, freight inflation, and polymer shortages are already affecting operations, while downstream impacts on laboratory consumables and CRO services are expected to intensify over the coming quarters. The overall impact will depend on the duration of disruption, but current data indicates that even a mid-term scenario results in significant cost escalation and operational pressure across pharmaceutical R&D.

References:

- Al Jazeera, “Shutdown of Hormuz Strait raises fears of soaring oil prices,” Mar. 3, 2026. [Online]. Available: https://www.aljazeera.com/economy/2026/3/3/shutdown-of-hormuz-strait-raises-fears-of-soaring-oil-prices

- CNBC, “How Strait of Hormuz closure can become tipping point for global economy,” Mar. 11, 2026. [Online]. Available: https://www.cnbc.com/2026/03/11/strait-of-hormuz-closure-shipping-economy-oil.html

- CNBC, “Worried about Strait of Hormuz inflation to come? The world economy has one word for you: Plastics,” Mar. 28, 2026. [Online]. Available: https://www.cnbc.com/2026/03/28/iran-war-strait-of-hormuz-petrochemicals-oil-plastics.html

- BASF SE, “BASF Pharma Solutions announces global price adjustment,” Mar. 30, 2026. [Online]. Available: https://www.basf.com/global/en/media/news-releases/2026/03/p-26-062

- F. Kansteiner, “API supplier BASF raises prices up to 20%,” Fierce Pharma, Mar. 31, 2026. [Online]. Available: https://www.fiercepharma.com/manufacturing/api-supplier-basf-raises-prices-20-response-rising-energy-costs

- BASF SE, “Caprolactam and polyamide price increase,” Mar. 23, 2026. [Online]. Available: https://www.basf.com/us/en/media/market-news-/2026/BASF-to-Increase-Prices-for-Caprolactam--Polyamide-Polymer--and-Copolyamide-in-North-America_03-23-2026

- SpecialChem, “Polyplastics-Evonik price increase,” Mar. 2026. [Online]. Available: https://www.specialchem.com/plastics/news/polyplastics-evonik-announces-price-increase-for-pa-and-peek-resins

- IOM3, “Strait of Hormuz closure affects chemicals and plastics exports,” Mar. 2026. [Online]. Available: https://www.iom3.org/resource/strait-of-hormuz-closure-affects-chemicals-and-plastics-exports.html

- ChemAnalyst, “Impact of Iran war on chemical prices,” Mar. 3, 2026. [Online]. Available: https://www.chemanalyst.com/NewsAndDeals/NewsDetails/chemanalyst-digest-how-iran-war-affects-chemical-prices-41348

- F. Kansteiner, “As Iran war squeezes Middle East drug shipments, experts warn of longer-term effects on U.S. manufacturing, generics,” Fierce Pharma, Mar. 2026. [Online]. Available: https://www.fiercepharma.com/pharma/iran-war-squeezes-middle-east-drug-shipments-experts-warn-longer-term-effects-us

- J. Grierson and D. Campbell, “Head of NHS England ‘really worried’ about medicine supplies,” The Guardian, Mar. 31, 2026. [Online]. Available: https://www.theguardian.com/business/2026/mar/31/medicines-run-out-weeks-nhs-england

- Roland Berger, “Managing the short- and long-term effects of Strait of Hormuz tensions,” Mar. 2026. [Online]. Available: https://www.rolandberger.com/en/Insights/Publications/Managing-the-short-and-long-term-effects-of-Strait-of-Hormuz-tensions.html

- D. Incorvaia, “The top 10 pharma R&D budgets of 2025,” Fierce Biotech, Mar. 30, 2026. [Online]. Available: https://www.fiercebiotech.com/special-reports/top-10-pharma-rd-budgets-2025

About The Author:

Mathini Ilancheran is a research manager, R&D, at Beroe Inc. She is an expert in procurement intelligence and industry analysis, specializing in strategic insights that help Fortune 500 companies make informed decisions. With a focus on global pharma, biotech, and medical devices, she brings deep expertise in value chain analysis, industry and technology trends, competitive intelligence, and strategy. Mathini has authored 37+ publications on R&D outsourcing, offering actionable perspectives that guide global enterprises in optimizing outsourcing practices, category management, and long-term planning.

Mathini Ilancheran is a research manager, R&D, at Beroe Inc. She is an expert in procurement intelligence and industry analysis, specializing in strategic insights that help Fortune 500 companies make informed decisions. With a focus on global pharma, biotech, and medical devices, she brings deep expertise in value chain analysis, industry and technology trends, competitive intelligence, and strategy. Mathini has authored 37+ publications on R&D outsourcing, offering actionable perspectives that guide global enterprises in optimizing outsourcing practices, category management, and long-term planning.