How Pfizer And Zoetis Launched One Of The Most Successful Spinoffs — Ever

By Rob Wright, Chief Editor, Life Science Leader

Follow Me On Twitter @RfwrightLSL

Spinning off a $4 billion biopharma business is no easy task. Integrated functions need to be separated, governance boards created, leadership teams assembled, and corporate headquarters established. And those are just a few of the tasks Pfizer faced when announcing the decision to spin off its animal health business back in 2012. A CEO also needed to be chosen for this soon-to-be, completely independent animal health company.

Enter Juan Ramón Alaix.

Since 2006 Alaix had been responsible for managing the Pfizer animal health business, a fact that made him the likely candidate for the new job, except for one thing — he had never been a CEO. That one missing ingredient has been known to turn what seems like a logical decision into a colossal catastrophe at some companies. Pfizer wasn’t about to take that risk. What follows is the story of how Alaix was groomed for his new role and how Zoetis turned into the world’s largest publicly traded animal health company with a per-share stock price outperforming that of its former parent.

STEP 1: PREPARE THE LEADER

“Now is the time to prepare yourself.” That’s what Pfizer CEO Ian Read told Alaix after the company’s board had recommended Alaix to be the CEO of Zoetis. “He wanted to make sure I continued growing the business while it was still part of Pfizer while also preparing for the separation and preparing myself for the new role,” Alaix recalls. Being the CEO of a public company is very different from running a division within a parent organization. Within a business unit there are some areas where you have complete control (e.g., commercial, R&D) and others where you have responsibility but rely on the parent company for support (e.g., financial reporting). While the head of a business unit might periodically provide an internal financial update, a CEO provides routine financial updates to internal and external stakeholders and often in very public forums. To help prepare Alaix to be Zoetis’ CEO, he undertook an aggressive 18-month training program.

The first part of his training was to work with Pfizer HR to define a personal development plan, through which it was determined he would benefit from being mentored by an experienced CEO from outside the company. Pfizer employed the services of Merryck & Co (an organization that specializes in leadership development), which put Alaix through a series of assessments to identify skill gaps. Merryck also provided him with a list of proposed mentors, from which Alaix chose the former CEO of a big European company. Meetings with his mentor began with a two-day retreat, after which they would usually speak on a monthly basis. Alaix found value in being able to bounce ideas off an outsider who could listen to his concerns and challenge him to think differently.

Another component of his CEO training involved a communications expert. Alaix had little experience with some of the communications required of a CEO (i.e., being comfortable doing print and TV interviews). “Before the IPO I was responsible for doing two road shows,” he shares. This was the first time he had such a responsibility, and his delivery of the Zoetis strategy to analysts, investor groups, and media would play an influential role in determining the company’s value. During his communication training he employed two different trainers to improve his skills in a variety of communication venues (e.g., small group presentations, keynote addresses, quarterly earnings calls). “But I had other help too, such as bankers and a lot of internal people who assisted in framing up the Zoetis strategy in a way easy for investors to understand,” he concedes.

STEP 2: PREPARE THE MARKET

For Alaix, the key to communication (and preparing the market) has been overpreparation. When it was time to actually execute his first real Zoetis road-show presentation, he had already done it dozens of times. “One of the road shows was geared toward the company IPO,” he states. “On February 1, 2013, Zoetis went public and we raised $2.2 billion.” This was when Pfizer sold approximately 20 percent of its stake in Zoetis. Three months later, Pfizer announced plans to spin off its remaining 80 percent company stake. “Preparing the market for Pfizer’s divestiture of its majority stake was what I discussed in the other road show.”

For each of these two presentations, Alaix had to deliver two types of information. First, he had to explain the difference between the human health and animal health industries. Second, he had to help investors understand why Zoetis was well prepared to be a completely independent animal health company. “Many of the people that were listening to us were analysts and investors very familiar with human health but had little knowledge about animal health,” he says. For example, many were surprised when Alaix described the animal health business as having nearly zero involvement by third-party insurance payers. “Our customers are veterinarians and livestock farmers, and when they make the decision to buy, they are also paying for their purchases.”

Another difference between animal health and human health is generic incursion. “In human health when you lose patent exclusivity, your revenue erodes by 90 percent within the first year,” he explains. “In animal health when a drug loses exclusivity, it might take five years to have an erosion of between 20 to 40 percent.” In fact, of Zoetis’ top 24 portfolio products, the average amount of time on the market is roughly 30 years. “Many are still growing in sales,” Alaix asserts. Animal health companies are less dependent upon the introduction of new products to compensate for generic incursion. Other differences include lower drug prices, as well as lower profits. “The average net gross profit in animal health is about 60 to 65 percent, which is a lot less than human health.” Generic companies are more interested in competing in the human health space because there is a significant opportunity to compete on price and still be profitable. “There is less pressure to lower animal health drug prices as there is less opportunity to do so.”

Another difference between the two industries is required infrastructure. “To reach customers [i.e., veterinarians] in animal health requires much more infrastructure,” Alaix contends. To effectively market and sell animal health products requires an extensive field sales force, which not only decreases animal health profitability, but also inhibits generic competitive entry. Consider this: About 14 percent of Pfizer’s 96,500 employees are members of its global field force, while approximately 29 percent (i.e., 2,610) of Zoetis’ 9,000 employees make up its global field sales force.

Another difference Alaix had to explain during his road shows was how animal health companies invest in R&D. “In our case, we balance our investing in new products while continuing to invest in our current portfolio of 300 product lines with new formulations, indications, combinations, and/or geographic expansions,” he explains. “Expanding the life cycle of our portfolio is a different R&D model that has the benefit of being much more predictable and less impacted by price.” This predictability is a hallmark of animal health. “For the last five years the animal health industry has had steady growth of between 5 to 6 percent, and is projected to grow at the same rate in the future,” he adds. In addition to being predictable, animal health is also resilient. “Even during the economic crisis of 2008 and 2009 [excluding the impact of currency exchange], the industry grew,” Alaix shares. “A highly stable and predictable industry is very attractive to certain investors.”

STEP 3: PREPARE THE COMPANY

When it came time to choose a name for the new company, they started with 1,000 options, winnowed the list to a top 10, and ultimately chose Zoetis, which is derived from the word zoetic, meaning “of or relating to life.” “We also liked the idea of the name beginning with a ’Z’ and an ’O,’ making it close to zoo, a word highly associated with animals,” Alaix says.

As part of the IPO preparation, Alaix also wanted to define the new company’s mission, vision, and culture. “We wanted to make sure these were not an extension of what we had been within Pfizer, but something closer to where we wanted to go as an independent company.

THE ZOETIS VISION

- Our products, services, and people will be the most valued by animal health customers around the world.

THE ZOETIS MISSION

- We build on a six-decade history and singular focus on animal health to bring customers quality products, services, and a commitment to their businesses.

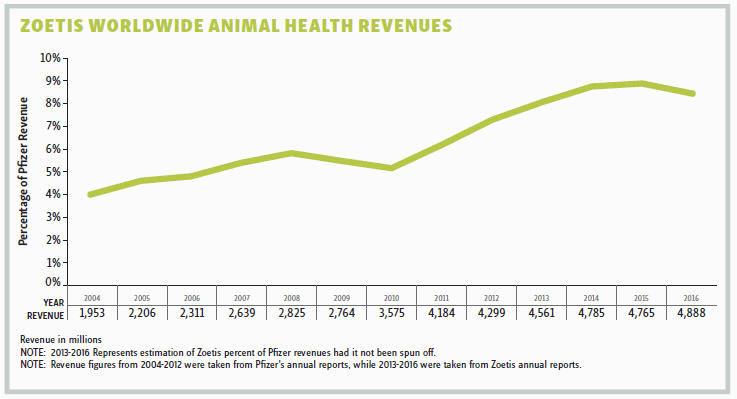

“Being a small company with a single focus on animal health, we saw the opportunity to create a culture with a strong sense of ownership,” he points out. As part of Pfizer it was very difficult for the animal health organization to “move the Pfizer needle” in terms of value (i.e., increasing earnings per share). “We only represented 5 to 7 percent of Pfizer’s total revenue. But as a much smaller independent company, a $5 million change after tax adds one penny in earnings per share at Zoetis.” Because Zoetis employees can see how what they do every day impacts the company’s value, Alaix believes they have a stronger sense of ownership than when they were part of Pfizer.

The company also wanted to eliminate silos, a message reinforced by an early lesson learned by Zoetis (see sidebar “Zoetis Experiences Early Growing Pains”). “When you are part of a big corporation as a business unit, some of the functions are within the business unit and others are outside of the business unit. As Zoetis, we had the opportunity for every colleague to have the same objective and focus, while eliminating that sense of territorialism.”

Preparing Zoetis to be a separate company also involved developing a corporate governance board and an executive leadership team. Alaix says he wasn’t concerned if these leaders had previous animal health experience. “I sought experience in various corporate functions that an organization operating as a business unit would typically lack.” Having been at Pfizer since 2003 provided Alaix the opportunity to identify and develop top talent existing throughout the Pfizer organization. But he had some other help. Prior to the IPO, Pfizer created an internal board to oversee the building of Zoetis, and Alaix met with this group monthly. The internal board included Pfizer’s CEO, Ian Read; Pfizer’s CFO, Frank D’Amelio; and several other top company executives.

While still part of Pfizer, the animal health division was tasked with conducting business as usual while also preparing for the future. As such, Alaix didn’t want to involve commercial or R&D in any part of the reorganization. “I wanted these two teams to remain intact and focused on what they were doing.” Other areas such as business development, finance, HR, IT, and manufacturing were tasked with defining what their future operating models should be as well as what tools they would need to operate independently from Pfizer. For example, a new enterprise resource planning (ERP) system from SAP was chosen with a plan of having it fully operational within 18 months of IPO. That’s an aggressive timeline, but Alaix knew that to have a successful separation, Zoetis needed to have full control of its operations.

The company also needed to figure out things such as appropriate department cost structures, best practices, and appropriate global geographic reach for a company of its size. For instance, as part of Pfizer, the unit operated in about 70 markets. “But we determined that as an independent company, continuing to operate in all of these countries in the same manner added complexity and cost without providing the right level of return,” Alaix explains. As part of an operational efficiency initiative begun in 2015, Zoetis moved 25 of these geographic locales from a direct-service model to a distribution-service approach. As the remaining 45 markets drove 95 percent of the company’s revenue, the move had minimal impact on Zoetis revenue.

During the efficiency initiative the company also sought to reduce its number of product offerings. “At Pfizer we were operating with 15,000 SKUs,” Alaix shares. “To be more efficient from both a financial and manufacturing perspective, we decided to eliminate about 5,000 SKUs.” This allowed Zoetis to have a better commercial focus on the products that really mattered, not only for its customers, but for the company itself.

Another primary objective was making sure that Zoetis operated as financially efficient as possible. Determining this took some time, and here’s why. Despite having a finance team in place, Zoetis was still initially dependent on Pfizer for its financial reports. “We knew the process of fully separating from Pfizer for some functions such as finance would take some time,” Alaix states. “But as we identified these opportunities early, we were able to fully implement our own finance system by the first quarter of 2016.” Alaix notes that other areas, such as HR, communication, and business development, moved toward independence almost from day one.

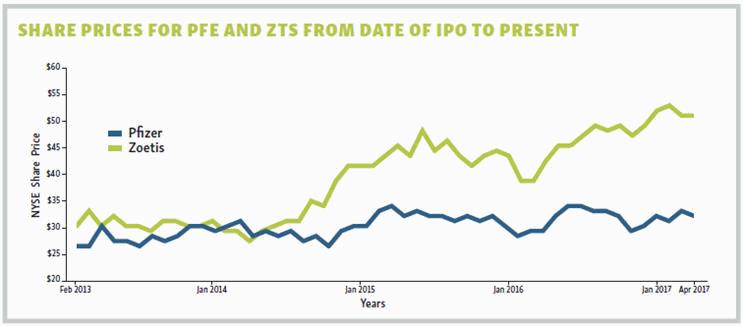

Despite some minor growing pains, the spinoff of Zoetis from Pfizer has been a remarkable success. In fact, there are probably a few Pfizer investors currently kicking themselves for not jumping at the chance to become Zoetis shareholders. For when Pfizer decided to sell its majority stake in Zoetis three months after the IPO, Pfizer shareholders were offered the opportunity to exchange $100 worth of company stock for $107.52 worth of Zoetis stock — a 7 percent discount. And while both companies continue to be highly successful, a side-by-side comparison shows that since Zoetis went public, the company’s share price has increased by more than 74 percent. During that same time period Pfizer’s share price has increased by a respectable 22 percent. That’s not a bad performance metric for a company with a first-time CEO.

SIDEBAR

ZOETIS EXPERIENCES EARLY GROWING PAINS

On May 16, 2013, Zoetis, which only three months earlier had been spun off from Pfizer as a completely independent company, got some very welcome news — an FDA approval for APOQUEL (oclacitinib tablet), which helps control severe itching associated with allergic dermatitis in dogs 12 months of age or older. But the drug launch did not go as smoothly as planned. “We made some conclusions based on market research that turned out to be false,” admits Zoetis CEO Juan Ramón Alaix. For example, market research indicated that the drug’s efficacy would be comparable to some existing therapies. In addition, veterinarians felt that the side effects of many of the existing therapies weren’t that severe, and something they could easily manage. “We had built our inventory based on this information,” Alaix shares. It wasn’t very far into the launch that Zoetis ran into a problem of being able to adequately supply the market. “Soon after launch we were getting market feedback that efficacy was much better than existing therapies,” he states. “And with regard to side effects of existing therapies being easily managed by vets, pet owners were the ones often having to deal with these, which they found to be problematic.” As a result, demand significantly exceeded Zoetis’ expectations.

The company worked toward ramping up supply, but manufacturing APOQUEL is fairly time consuming. “It takes about a year, not just a couple of months,” Alaix attests. “It starts with the ordering of registered materials, which can take several months when you factor in shipping, clearing customs, etc. Then the production of the API, which is another seven to eight months, before we move on to finished goods.” As a result, for many months Zoetis had some very frustrated customers wanting to use APOQUEL. High demand and lack of product supply created a significant negative market reaction. “It is very disappointing for any organization to have such a good product and not be able to meet customers’ expectations.”

One of the goals when first formulating the Zoetis spinoff was to create a corporate culture that lacked silos. The pain experienced from this failure to supply customers reinforced this desire when it came to preventing this as a future problem. “Improving market research was certainly an opportunity,” Alaix stresses. “But there were other learnings from APOQUEL.” For example, Zoetis learned that the commercial organization didn’t fully understand the complexity of APOQUEL manufacturing. “When we are developing a process, it needs to work in a very integrated fashion,” Alaix explains. “All functions need to be well aligned before launch [i.e., R&D, commercial and manufacturing].” Today, when Zoetis has a product in development, rather than involve commercial or manufacturing during later stages, the company includes these disciplines much earlier, so everyone understands the product’s needs and volumes. “To reduce risk and have better coordination means all functions have to have full information about all the different activities and decisions being made.”

The company now also develops best- and worst-case scenarios, so they can have plans in place to react quickly and appropriately. One such plan was used when launching CYTOPOINT, a sterile liquid containing a monoclonal antibody (mAb) for treating dogs with atopic dermatitis. “We built the capabilities to produce our own mAbs,” Alaix shares. “I believe this has put us in a situation where we will be able to meet all of our customers’ needs, even if demand exceeds our initial projections.”