How Pharma Go-To-Market Strategy And Launch Readiness Are Transforming

By Qasim Zaidi, Eduardo Schur, and Aayush Anand

Speed alone no longer guarantees success; here’s what matters most in today’s launch environment.

In today’s launch environment, order of entry (OOE) isn’t destiny. Many brands still anchor strategy to first-to-market or first-in-class thinking, yet over 50% of U.S. launches miss initial sales forecasts because they are designed for today’s value signals, not the signals that will matter at launch and beyond. The imperative is to build a go-to-market (GTM) model that meets the real unmet need at launch, where prescribers, patients and payers will assign value, and that can scale quickly.

Across therapeutic areas, a large share of products miss initial forecasts for predictable reasons: overweighting clinical novelty, underweighting access and patient experience friction, and assuming homogeneous customer behavior. Forecast models frequently over‑index on efficacy and under‑index on friction such as prior authorization, affordability, site‑of‑care setup, or convenience and prescriber/patient time burden. Brands arrive with compelling data but insufficient proof of differentiated value in use that drives trial, adoption and persistence.

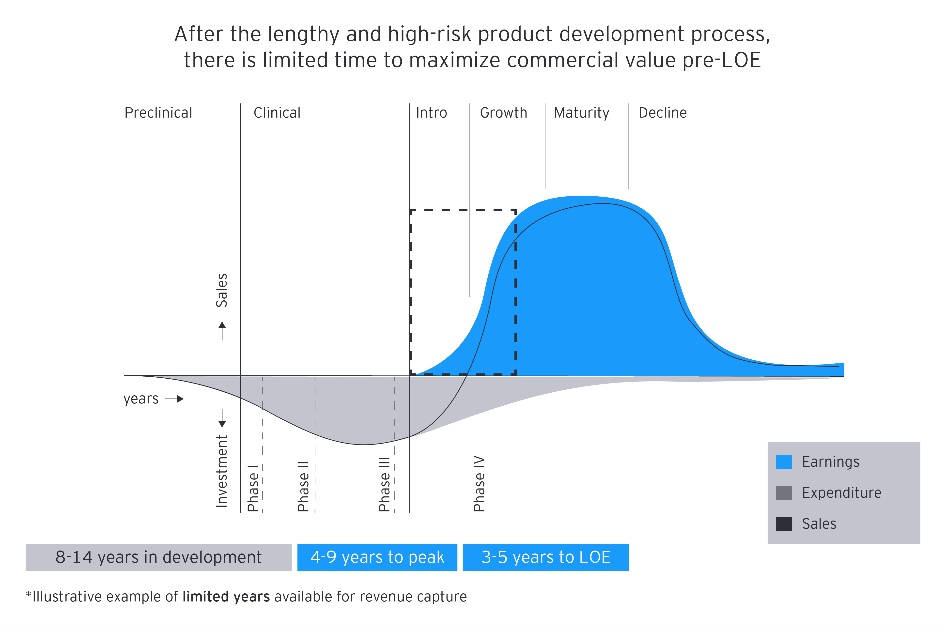

Accessibility description: The graphic illustrates how a long development timeline leaves only a short period to generate meaningful sales before loss of exclusivity. A blue curve shows sales rising after launch and later declining, while a grey area represents high early expenditures that decrease over time across the preclinical, clinical, introduction, growth, maturity and decline phases.

Below, we explore the foundational forces reshaping GTM strategy in the pharmaceutical industry. We examine why relevant differentiation, robust evidence and consumer-grade patient experiences have become critical to outperforming speed and novelty. Understanding these market shifts can help companies design GTM models that address real unmet needs and scale effectively in today’s complex, competitive landscape.

Six Powerful Forces: Why Innovative GTM Matters More Than Ever

While a forecast miss merely indicates a mismatch in expected outcomes, it serves as a clear signal that a more innovative and adaptive GTM approach is urgently needed. Today, six powerful forces are raising the bar for launch success and making GTM innovation non-negotiable:

- Consumer-grade expectations. Today’s patients have expectations beyond clinical efficacy. They demand intuitive onboarding, transparent affordability, and digital self-service options that mirror their seamless experiences in other industries, like retail. Proactive, personalized support is now a baseline, not a differentiator. Healthcare providers (HCPs) seek low-friction engagement, streamlined administrative processes, and relief from burdensome paperwork. Winning brands recognize that customer experience is a core product attribute, designing seamless journeys from e-prescribing to fulfillment, integrating real-time benefits verification and prioritizing human-in-the-loop support for both patients and providers. This shift elevates patient and provider satisfaction, driving adoption and persistence.

Source: Unleashing digital momentum to shape the future of healthcare

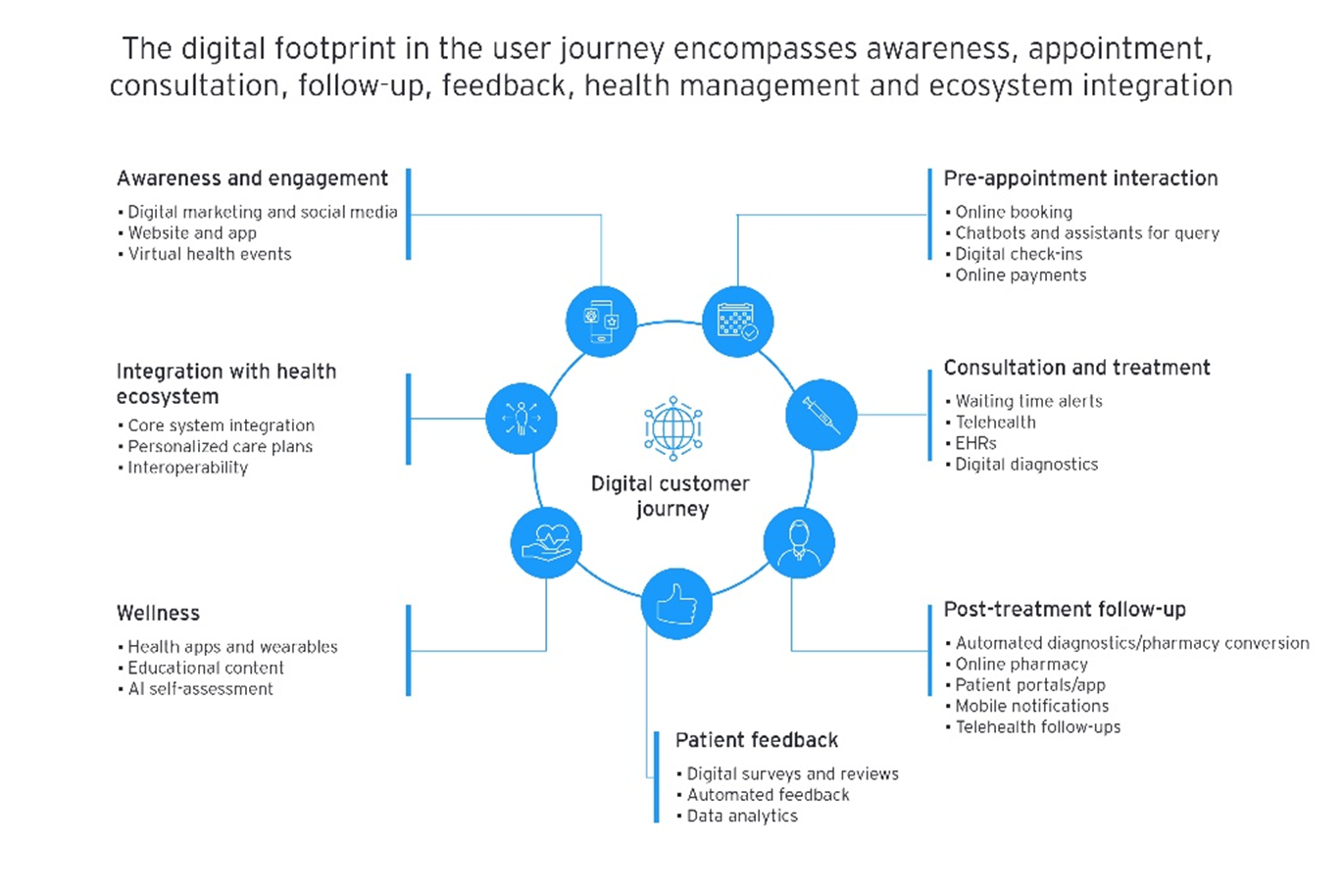

Accessibility description: This graphic illustrates the digital touch points that shape a patient’s end‑to‑end healthcare journey, emphasizing that healthcare experiences are increasingly connected and enhanced through digital interactions at every step. At the center is the “Digital customer journey,” surrounded by icons and labeled categories showing how digital tools support each stage — from awareness and appointment booking to consultation, treatment, follow‑up, wellness, patient feedback, and integration with the broader health ecosystem. Each category lists examples such as digital marketing, online booking, telehealth, diagnostics, patient portals and automated feedback.

- Shift to therapies for prevalent disease areas. In the recent past, the industry saw a pronounced shift toward specialized therapies for rare diseases, precision oncology, and complex modalities, where success depended on site-of-care enablement and complex patient services enablement. That dynamic is changing. In the life sciences space, the pendulum is swinging dramatically from niche specialty drugs to large-scale therapies for chronic conditions (e.g., obesity, immunology, and mental health), driven by breakthrough innovations and unprecedented demand. U.S. prescription drug spending jumped by 11.4% in 2024 — adding roughly $50b to the total pharmaceutical drug spend. GLP-1 agonists for diabetes and obesity were key contributors, accounting for nearly 29% of that growth. Neurology has followed a similar trajectory. The rising prevalence of anxiety and depression has driven a substantial increase in antidepressant prescriptions, particularly among adolescents and young adults, where prescription rates climbed by 63% following the onset of the pandemic. In many parts of the U.S., more than 10% of prescriptions in 2022 were for anxiety or depression. This shift introduces a new challenge: delivering on consumer-grade expectations at scale. Unlike niche therapies, mass-market products must deliver seamless experiences across large, diverse populations and multiple channels: retail, specialty, telehealth and integrated care networks. Brands that fail to meet these expectations risk losing share quickly in highly competitive, high-volume, share-of-voice categories.

- Escalating R&D costs. R&D costs continue to rise while therapeutic categories grow more competitive and payer budgets tighten, creating unprecedented pressure to enable each new therapy to deliver clear and measurable value. According to recent estimates, the average cost of bringing a new drug to market is about $2.6b, with the process of drug development typically taking 10 to 15 years and with an FDA approval rate of only about 12%. As investment requirements increase across discovery, development, manufacturing, and evidence generation, organizations must take a more disciplined approach to demonstrating clinical and economic impact from day one. Early, cross-functional planning between clinical, medical, health economics and outcomes research, and market access teams is essential to align evidence strategies with the data payers require to make informed coverage and utilization decisions. Robust insights into comparative effectiveness, total cost-of-care implications and real-world outcomes help stakeholders understand where a therapy can create the greatest value relative to existing options.

- Intensifying competition within and beyond class. Competition is intensifying because the basis of differentiation is expanding beyond core clinical attributes. Companies increasingly compete through care model integration, patient support, and channel execution. For example, Pfizer’s collaboration with Sidekick Health illustrates this shift: Providing adherence and behavior-support services alongside therapy led to improvements in adherence for 83% of users and a 40%–50% reduction in symptom severity in feasibility studies. This and other similar digital tools are demonstrating the value of and increasing expectations to leverage a broader suite of integrated services to improve patient outcome tools. Similarly, hybrid HCP engagement has become a structural requirement, with virtual and asynchronous channels preferred by most prescribers. These dynamics reset the competitive bar: Success hinges less on clinical data alone and more on shaping the ecosystem, educating on disease pathways, supporting diagnosis, integrating patient services, and executing with precision. Companies that move early to define expectations and customer experience create durable advantage, regardless of first- or fast-follower positioning.

- Policy and payer dynamics. Evolving price negotiation frameworks and assertive management from payers and the governments are shifting value demonstration from a downstream hurdle to an upstream design input. Access strategies must now incorporate fit-for-purpose evidence, outcomes-linked contracting and benefit design navigation, with prior authorization (PA) step-down tactics embedded in the brand experience. Companies must proactively engage with payers to align on value drivers and create broad, sustainable access. This proactive approach is essential for long-term success in a complex policy landscape. The new environment also demands smarter pricing and market access strategies, synchronized with launch and indication sequencing decisions to avoid being disadvantaged through Inflation Reduction Act (IRA) and Most Favored Nation (MFN) pricing constraints. Selecting which indication and where to launch first is no longer just a commercial choice; it’s a strategic safeguard against cascading price pressures across markets. This proactive approach is essential for long‑term success in a complex policy landscape.

- Acceleration and expectation from GenAI and agentic AI. With 48% of organizations planning to devote at least a quarter of their budgets to AI, the mandate is clear: scale with purpose. Pharma leaders are embedding GenAI and agentic AI into workflows, including leveraging AI for hyper-personalized next-best-action engagement, dynamic targeting, and rapid feedback loops, raising the bar for agility and responsiveness. Beyond customer-facing applications, GenAI is reshaping core launch operations, streamlining the development of dossiers, payer submissions, sales training materials and advanced analytics that once required lengthy manual cycles. Companies are also deploying tools like automated first-pass medical, legal and regulatory (MLR) engines that identify compliance risks early and reduce review bottlenecks so that content can scale without compromising quality or governance. Reports indicate that pharma companies implementing MLR automation have achieved a 57% reduction in review cycle times and a 55% drop in time spent in review meetings. Even in terms of drug development, research suggests that AI involvement can reduce clinical trial costs by up to 70% and timelines by 80%. Agentic AI is already moving from concept to practice in pharma: Platforms such as Veeva Vault are embedding AI agents directly into clinical, regulatory, safety, quality, medical, and commercial applications to assemble documents, detect missing metadata, summarize deviations, and drive content through predefined workflows with minimal human intervention. Similarly, life sciences leaders are piloting autonomous agents that triage medical inquiries, early signals that launch-critical processes are shifting from isolated GenAI tools to end-to-end, agent-driven workflows. However, speed without strategic direction can create noise and misalignment. The most successful organizations pair AI-enabled agility with future-back strategy so that evidence, messaging and services are built for the market realities that will exist at launch.

Source: Artificial Intelligence at the helm: revolutionizing the life sciences sector

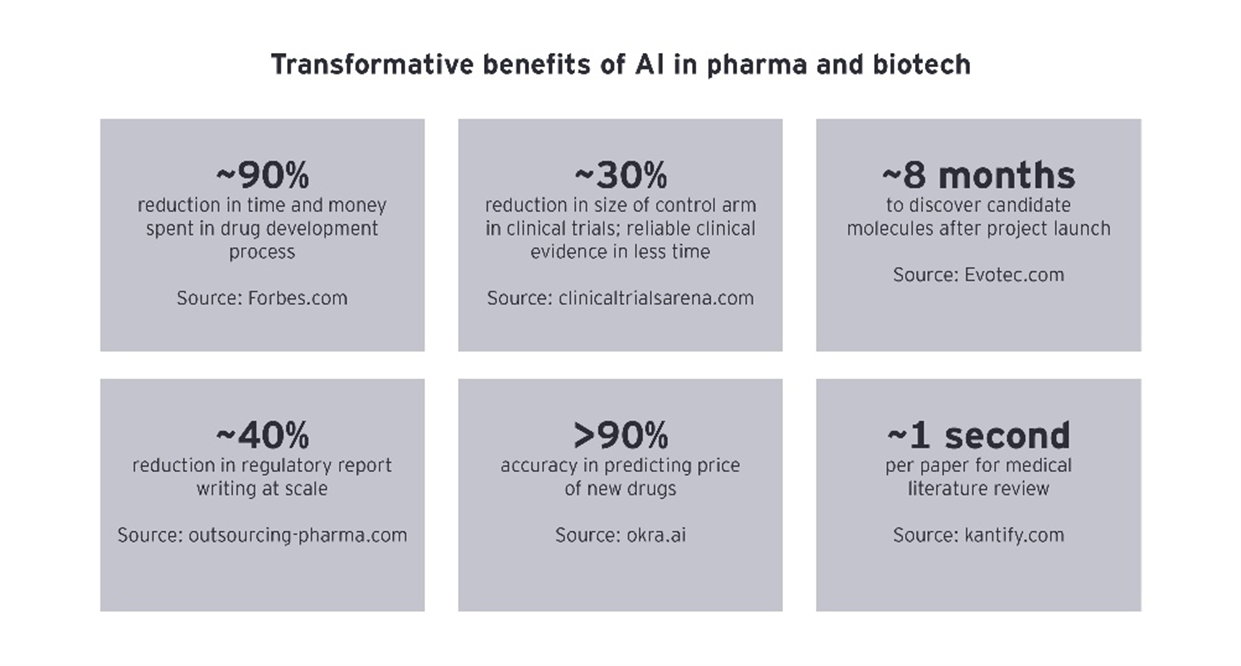

Accessibility description: This graphic shows six statistics illustrating how AI significantly speeds up and reduces the cost of work in pharma and biotech — cutting drug development time and trial size, accelerating molecule discovery, improving report writing efficiency, boosting drug‑price prediction accuracy and enabling rapid literature review.

Altogether, these six market forces are redefining GTM requirements for a brand’s success.

Navigating The Challenges: Case Studies For GTM Success

Let’s focus on how late entrants in key therapeutic areas have leveraged differentiated clinical profiles, superior patient experiences and innovative access strategies to disrupt incumbents and capture significant market share. We intentionally include late entrants, since the benchmark for success is higher, and intentionally exclude oncology and immunology, where multi-indication launches, combination strategies, and fundamentally different go-to-market dynamics make direct comparison less instructive for the purposes of this framework.

Each example provides a distinct case of a therapy approved second, or even later, achieving meaningful commercial success through differentiated clinical profiles, superior patient experience, access strategy, or operational excellence. Our analysis draws on the lessons from these markets to understand what enables a late entrant to overcome first-mover advantages and capture significant share.

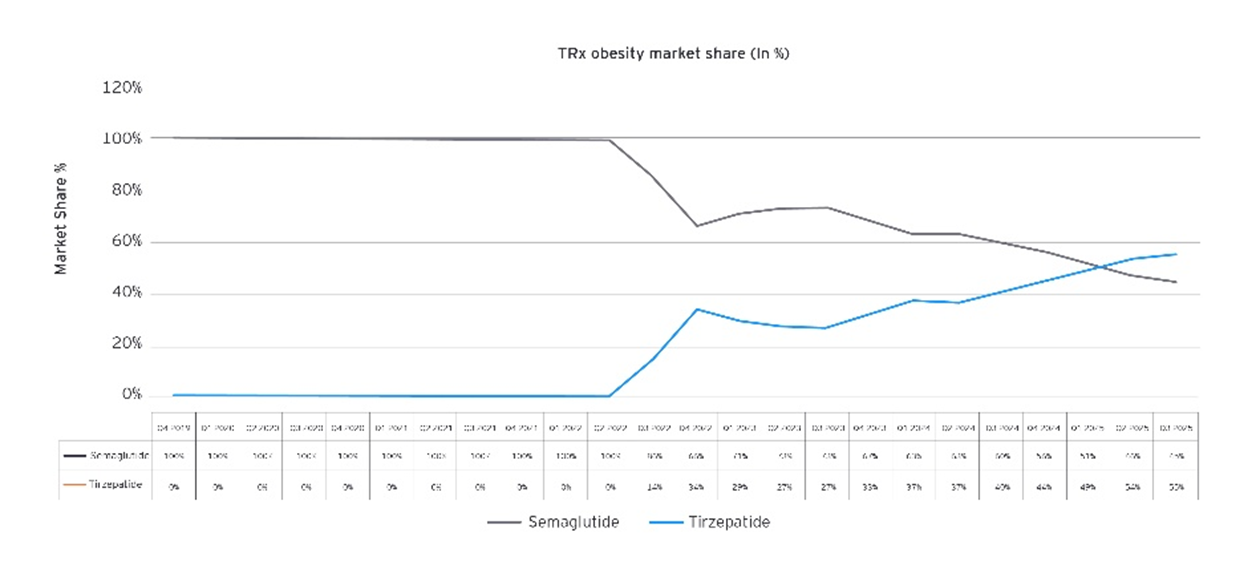

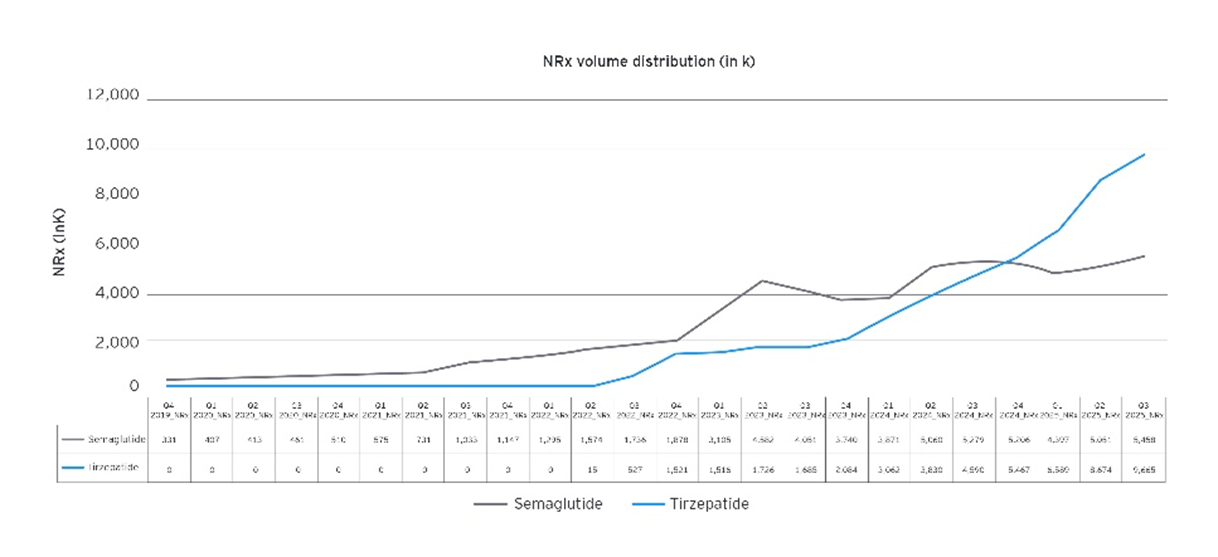

Consider tirzepatide in obesity: Despite semaglutide’s head start, tirzepatide leveraged targeted go-to-market tactics to capture and ultimately surpass semaglutide’s market share. A similar pattern emerged in ophthalmology, where faricimab replaced ranibizumab as the key branded product in the manufacturer’s portfolio and captured significant market share from aflibercept through innovation and compelling stakeholder engagement. This trend is not isolated: Myasthenia gravis, a rare disease, provides another example where a later entrant outperformed early competitors. As we explore the following drivers of launch success, we’ll highlight how each of these competitors captured share in their respective market.

Source: EY analysis

Accessibility description: This graphic shows how tirzepatide grew both obesity market share and new prescriptions over time, eventually overtaking semaglutide. Semaglutide starts with 100% market share and higher early prescription volume, but its growth levels off as tirzepatide gains traction and becomes the leading treatment by 2025.

What Drives GTM Success?

As the pharma landscape evolves, understanding the key drivers of GTM success becomes crucial for companies aiming to thrive in a competitive environment. Below, we delve into the essential elements that shape effective GTM strategies, exploring how companies can navigate these dynamics to achieve lasting impact.

Market shaping: the early advantage

Market shaping is often thought of as essential for first entrants and optional for late entrants, who often attempt to ride the coattails of class leaders. However, decision criteria tends to harden quickly, making it challenging to reshape the market’s perception. Companies that underinvest early in market shaping rarely recover, and research shows that roughly 80% of new drug launches fail to materially improve their initial sales trajectory within the first six months to two years, irrespective of order of entry. To win, companies must shape the market early by defining valued attributes, enabling the ecosystem, and setting economic expectations, irrespective of launching second or third. This involves reframing the value proposition from maximal efficacy to reliable and scalable outcomes, socializing endpoints and outcomes with key stakeholders before pivotal trials, preparing sites of care and specialty pharmacy flows for launch, and introducing bridge programs and outcomes assurances to lower switching barriers.

Case example: Efgartigimod employed a bold market-shaping tactic in a rare disease category traditionally driven by specialist relationships and IV center economics. The manufacturer adopted an unconventional pricing model, setting the price at 50% less than the eculizumab (standard of care) list price, alongside unusually prominent direct-to-consumer (DTC) marketing in a market where patient awareness had historically been near zero. By normalizing patient-driven demand and later advancing self-injectable formats, they challenged entrenched assumptions that rheumatologists and neurologists prefer IV therapies because of buy-and-bill incentives. This strategy not only expanded the addressable market but also redefined expectations for convenience, autonomy, and the perceived value of therapy in IgG-modulating treatments.

Go-to-market by design: Where to play

Commercial success begins with thoughtful segmentation, identifying where to play by analyzing care settings, channels, prescriber archetypes and patient phenotypes. Understanding what customers truly want through hyper-personalized insights, including clinical outcomes, convenience, affordability or support, is essential for shaping both product and service offerings. Companies should invest early in market research and stakeholder engagement to uncover unmet needs and evolving preferences so that their launch strategy resonates with the intended audience. Early positioning is critical; brands must define their unique value proposition and target segments well before launch to achieve relevance and differentiation.

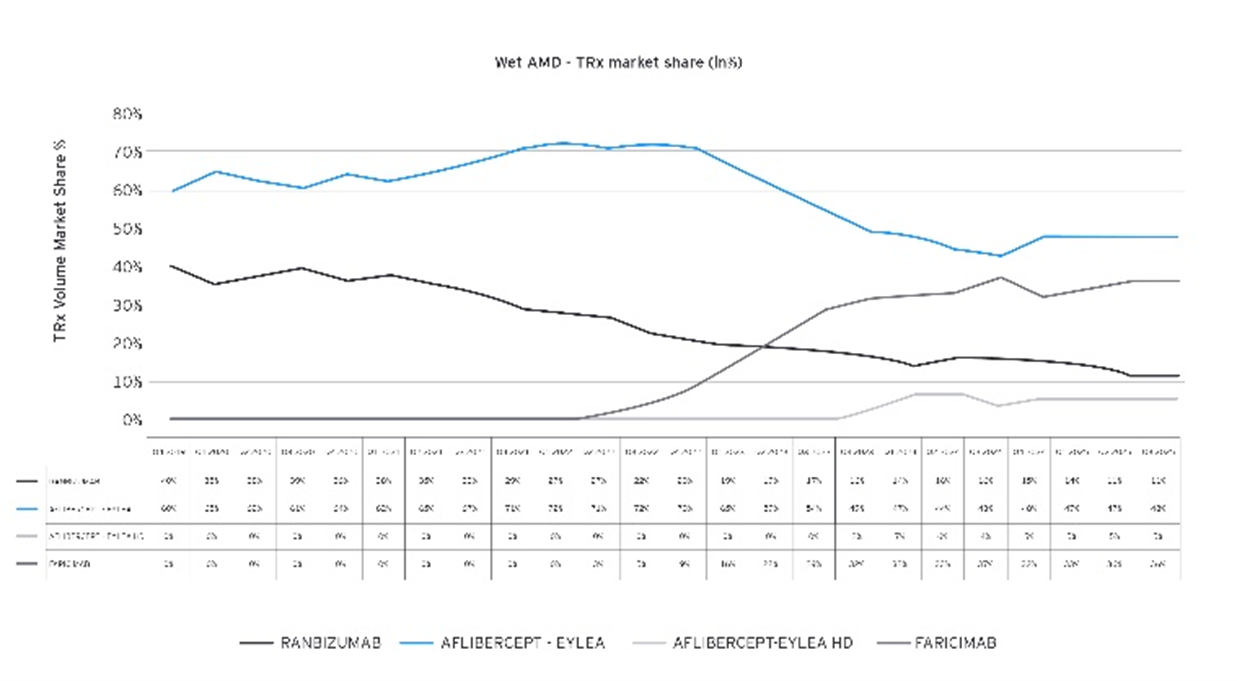

Case example: Faricimab’s manufacturer amplified its adoption by leveraging DTC strategies, using targeted digital campaigns and messaging focused on active lifestyles (“fewer clinic visits, same results”) to build patient awareness and interest. These lifestyle benefits were identified as critical drivers for patients and payers, making faricimab an attractive option for treatment. Faricimab differentiated itself amid aflibercept’s familiarity and convenience by offering clinically superior (dual mechanism of action) and patient-centric innovations such as extended dosing intervals, prefilled syringes and one-hand administration to reduce the treatment burden for patients and providers. On the provider side, faricimab focused on busier clinics looking to open capacity for more valuable services (like surgery) and optimize workflow.

Source: EY analysis

Accessibility description: The graphic shows total prescription (TRx) market share for treatments used for Wet Age‑Related Macular Degeneration (Wet AMD) from 2019 to 2025. Aflibercept (Eylea) begins as the clear market leader but declines steadily over time, while Ranibizumab also decreases. Faricimab, introduced later, rises quickly and becomes a major competitor by 2025. Eylea HD shows a small but gradually increasing share. Overall, the chart illustrates the market shifting from older therapies toward newer options, driven largely by Faricimab’s rapid growth.

How to win: Securing market access

Securing market access should be treated as a strategic priority from the outset, not as a post-approval hurdle. This means proactively designing access pathways, optimizing distribution and aligning benefit design and economic instruments to minimize friction for both providers and patients. Early engagement with payers and stakeholders is essential to anticipate potential barriers and put access solutions in place before launch. By confirming that eligible patients and providers are supported through pre-launch education and access planning, companies can reduce friction at launch and enable faster therapy initiation once approval is granted. Additionally, through integration of market access planning into the earliest phases of product development, companies can better align clinical and commercial strategies, ultimately accelerate uptake and maximize impact at launch.

Case example: Ophthalmology has rapidly consolidated under private equity, with about 40% of physician practice deals from 2017 to 2021 driven by PE ownership. As these platforms push for scale and throughput, manufacturers now compete on alignment with PE-managed clinic economics, not just clinical differentiation. Faricimab has gained momentum by positioning longer dosing intervals as a lever to expand capacity and improve physician workflow. Aflibercept’s manufacturer responded with a high-dose formulation to retain share and deliver stronger patient and clinic economics. Both brands are now shaping their value propositions around the priorities of clinics: lower injection burden, smoother patient flow and improved capacity utilization.

Case example: While semaglutide’s obesity-indicated version launched at a $1,300-per-month price point, triggering affordability and insurance barriers, its competitor priced tirzepatide diabetes and anti-obesity indication versions at about $1,080 per month, simplifying the pricing for patients and further differentiating itself with deep out-of-pocket discounts. Additionally, tirzepatide’s manufacturer introduced single-dose and lower-dose formats specifically designed for the self-pay market, giving patients additional agency and optionality on how to access their drug.

Supply chain and scale as a competitive advantage

Across the industry, supply chain readiness is becoming a decisive factor not only in launch execution but in sustaining competitive momentum. Recent visibility into high-profile regulatory setbacks, such as aflibercept HD formulation delays tied to fill-finish or device-component manufacturing issues, illustrates how even strong clinical assets can face headwinds when dependent on vulnerable production nodes. For example, challenges in scaling or qualifying third-party manufacturing partners for critical components, such as prefilled syringes, can slow market uptake and limit a brand’s ability to compete on convenience and delivery innovation. In contrast, therapies with flexible, unconstrained manufacturing footprints, such as orforglipron for obesity, are built for rapidly expanding categories with high demand variability, allowing them to capture market opportunities immediately rather than having to ration supply or navigate repeated resubmissions. As demand surges become less predictable, resilient, diversified and inspection-ready manufacturing networks are emerging as true competitive differentiators, shaping both short-term launch trajectories and long-term franchise durability.

Scaling from a smaller wedge win to a market mover involves out-investing in commercialization where it drives adoption and persistence, extending switching economics through bridge programs and assurance constructs and reducing customer burden. Expansion to adjacent segments should be guided by insights gained from the initial wedge, while operational scaling requires increasing specialty pharmacy network capacity, tightening data loops and enhancing concierge support. Throughout growth, it is essential to maintain price integrity and service quality.

Case example: Tirzepatide’s manufacturer reshaped access to obesity drugs by moving beyond the specialty-pharmacy model and building a direct-to-patient ecosystem. The company launched a platform connecting patients with independent clinicians and telehealth prescribers, enabling transparent self-pay pricing and reducing friction in starting therapy. Partnerships with major telehealth groups and online pharmacies added fast home delivery and 24/7 pharmacist support, setting a new expectation for convenience. Most recently, a collaboration with the nation’s largest value retailer brought single-dose vials into 4,600 in-store pharmacies, making tirzepatide one of the first obesity medicines with true retail pickup and broad consumer reach.

Creating engagement at launch

After investing in segmentation, access, evidence and patient experience, leading brands further differentiate themselves through orchestrated launch experiences that capture stakeholder attention. By using storytelling and coordinated multichannel engagement, they can ride hype cycles and create an emotional connection within the bounds of compliance, transforming a therapy introduction into a moment of high engagement and sustained interest. Pharma companies can achieve this by aligning cross-functional teams early (medical, commercial, compliance, supply chain) to co-create narratives, digital content and engagement plans that resonate authentically with each stakeholder group.

Case example: Timed press releases, retail announcements, targeted DTC advertising and published content on their website enabled tirzepatide to maintain a steady stream of high-visibility headlines, which focused more on access, scale and affordability — going beyond medical and clinical narratives.

The drivers of launch success are shifting

In emerging classes with high unmet needs, efficacy and clinical impact are crucial. Early access, advocacy from key opinion leaders and clear clinical guidance are essential for adoption. As markets transition and fast followers emerge, evidence that de-risks switching — such as head-to-head trials, patient-reported outcomes and real-world evidence — becomes critical. Coverage breadth, onboarding support and site-of-care readiness further enable growth. In mature therapeutic classes, convenience, access design, patient experience, direct-to-consumer engagement and value for price become the dominant factors. Ultimately, value in use, speed to therapy, low administrative burden and affordability determine which products win market share.

Common pitfalls to avoid

As companies navigate the complexities of launching new therapies, it’s crucial to be aware of potential missteps that can undermine their efforts. Launch teams should remain vigilant against the following challenges — some of the most common pitfalls — which can derail even the most promising strategies:

- Under-investing in evidence generation, building for access and patient experience

- Targeting the average customer instead of a high-need micro-segment

- Shaping the market too late after decision criteria have hardened

- Generating data that is not valued in real-world decisions

- Scaling too broadly or too quickly, putting service and price integrity at risk

The pharmaceutical launch environment is no longer defined by speed alone. Success now depends on anticipating what prescribers, patients and payers will value at launch and building strategies accordingly. Organizations must reframe launch readiness around differentiation, evidence, and experience: invest early in market shaping; design consumer-grade experiences that reduce friction; and align evidence generation with payer and real-world needs. Companies that embrace these principles will position themselves to win in an increasingly competitive market. Ultimately, not being first to market means you must be first to deliver what the market truly values at the time of your launch.

About The Authors:

Qasim Zaidi, Managing Director, Life Sciences Commercial Strategy, Ernst & Young, LLP

Qasim Zaidi, Managing Director, Life Sciences Commercial Strategy, Ernst & Young, LLP

Qasim Zaidi is an Executive Director in the Commercial Strategy lead for EY Life Sciences, advising clients on brand and portfolio go-to-market, functional and enterprise operating model transformation, and capability transformation initiatives. His focus areas are market access, marketing, and medical affairs. He has 20+ years of experience in advising his clients and prior to joining EY, he served as a market access leader for BMS’s immunology and cardiovascular franchises.

Eduardo Schur, Principal, Commercial Strategy and R&D, Ernst & Young, LLP

Eduardo Schur, Principal, Commercial Strategy and R&D, Ernst & Young, LLP

Eduardo Schur is a Partner and the Life Sciences Commercial and R&D Lead at EY US, advising biopharma and biotech companies on commercial strategy, R&D, and product launch execution. Prior to EY, he served as Global Leader of the Guidehouse (formerly Navigant) Life Sciences Practice and held multiple senior commercial leadership roles at Bristol‑Myers Squibb, including Vice President of Marketing. He is also a member of the faculty at the Edward J. Bloustein School of Planning and Public Policy at Rutgers University.

Aayush Anand, Life Sciences Commercial Strategy, Business Consulting, Ernst & Young, LLP

Aayush Anand, Life Sciences Commercial Strategy, Business Consulting, Ernst & Young, LLP

Aayush Anand is a Senior Manager in EY’s Life Sciences Commercial and R&D practice with experience spanning Oncology, Hematology, Immunology, CVRM, Cell & Gene Therapy, Neurology, Pain, and Women’s Health. His work focuses on portfolio and pipeline strategy, launch planning, and enterprise‑level decision‑making for biopharma organizations. Previously at ZS Associates, Aayush supported global pharma and MedTech companies across pipeline and launch strategy, commercial due diligence, and forecasting.

Contributors:

Aman Bhatnagar, Manager, Strategy & Transactions, EY GDS

Drew Crum, Business Consulting, Ernst & Young, LLP

The views reflected in this article are the views of the author and do not necessarily reflect the views of Ernst & Young LLP or other members of the global EY organization.