Outsourcing And The Oral Solid Dose – Will Challenges Lead To New Patterns Of Outsourcing?

By Kate Hammeke, director of marketing intelligence, Nice Insight

Historically, the prevailing dosage form for small molecule drugs has been the oral solids. They are cost-effective, have a proven safety and efficacy record over the course of more than a century, and from a consumer perspective, the familiarity of this form promotes patient compliance. But while tablets are still the most popular means for taking medicine, current industry information indicates that a significant portion of new chemical entities present solubility challenges, forcing developers to look at alternatives more frequently. As one industry observer put it, a lot of the low-hanging fruit has gone, so discovery is increasingly focused on niches and more complex approaches. So the question is how innovative dosage forms will develop, and what this means for contract manufacturers.

Historically, the prevailing dosage form for small molecule drugs has been the oral solids. They are cost-effective, have a proven safety and efficacy record over the course of more than a century, and from a consumer perspective, the familiarity of this form promotes patient compliance. But while tablets are still the most popular means for taking medicine, current industry information indicates that a significant portion of new chemical entities present solubility challenges, forcing developers to look at alternatives more frequently. As one industry observer put it, a lot of the low-hanging fruit has gone, so discovery is increasingly focused on niches and more complex approaches. So the question is how innovative dosage forms will develop, and what this means for contract manufacturers.

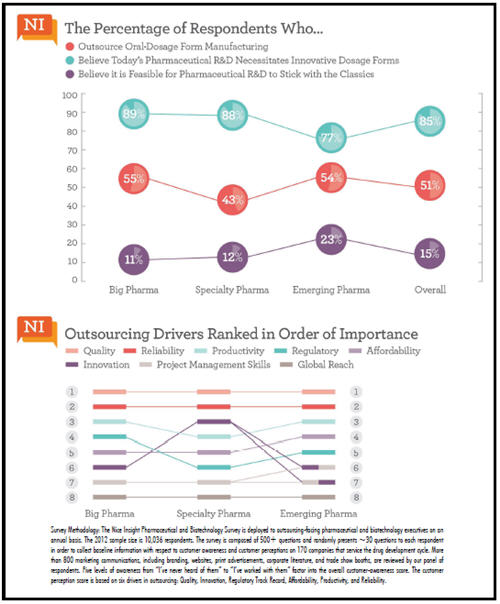

Nice Insight’s survey asks buyers of CMO services about their practices in outsourcing solid oral-dosage forms. Responses tell us that, on average, 51% of respondents from pharmaceutical companies outsource solid dose manufacturing. Big Pharma (55%) and emerging pharma respondents (54%) skew the average higher, as they are more likely to engage a CMO for manufacturing than specialty pharma respondents (43%).

However, fewer than one in five believes that traditional tablets will meet all the delivery needs of its drug development pipeline. About 85% state that innovative dosage forms — including controlled-release, fast-dissolve, or combinatorial drugs with multiple APIs — will be essential in coming years. Interestingly, almost a quarter of respondents from emerging pharma believe they can stick with the classics, but only 1 in 10 Big Pharma and specialty respondents believes traditional oral solid dose will continue to meet its needs. This may be an indication of the balance of what these companies are working on, or it could simply be indicative of experience.

The Drivers That Influence Outsourcing

Differences among these three groups carry over to the drivers that influence their decisions to outsource as well. Quality and reliability consistently take the top two positions across the board, but priorities diverge from there. Big Pharma ranks productivity next, followed by regulatory, affordability, and innovation. Emerging pharma also ranks productivity third, but follows with affordability, regulatory, and innovation. Specialty Pharma bucks the trend by placing innovation third, followed by productivity, affordability, and regulatory.

Preferred CMOs

With diverging drivers for outsourcing, it is perhaps no surprise that they have varying preferred CMOs for oral solid-dose manufacturing. However, Next Pharma and Catalent both appear in the top three in two buyer categories. Big Pharma’s descending order of preferred CMOs are Boehringer Ingelheim, Next Pharma, and AMRI. Specialty Pharma respondents identified Wellspring, Catalent, and AbbVie (formerly Abbott Contract Manufacturing) in the top spots. The top three among emerging pharma respondents are Catalent, Glatt, and Next Pharma.

There are important similarities among these CMOs — namely, that each possesses technologies and/or formulation skills focused on solving broader solubility challenges. Proprietary technologies and advanced formulation capabilities will likely cement pharmaceutical innovators into long-term relationships, and if they are seeking strategic relationships as industry trends suggest, they may be looking for CMOs that can offer the flexibility of traditional solid-dosage solutions as well as innovative dosage forms.

There is no doubt that solid dosage will remain relevant wherever it is feasible due to its cost benefit and relative lack of challenges, but innovative routes will not only address formulation challenges, they will also be relevant to other healthcare trends and future possibilities, such as efficacy breakthroughs and changes in patient expectations, behavior, and lifestyle.

If you want to learn more about the report or about how to participate, please contact Nigel Walker, managing director, or Salvatore Fazzolari, director of client services, at Nice Insight by sending an email to niceinsight.survey@thatsnice.com.

If you want to learn more about the report or about how to participate, please contact Nigel Walker, managing director, or Salvatore Fazzolari, director of client services, at Nice Insight by sending an email to niceinsight.survey@thatsnice.com.